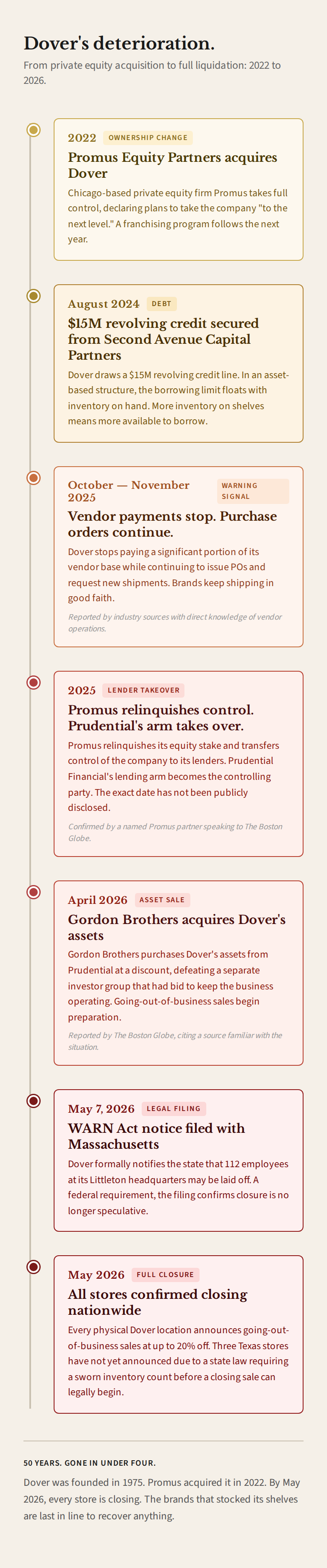

It is over. Dover Saddlery is closing every physical location in the country. Not a subset of stores. Not a strategic contraction. All of them.

If you have been waiting for clarity, this is it. The going-out-of-business sales now running at Dover locations nationwide are not a turnaround strategy. They are the final act of a liquidation managed by Gordon Brothers, a firm that specializes in exactly this: buying distressed retail assets at a discount and recovering as much as possible before the lights go off.

There are a few things about this liquidation that deserve more explanation than they have received. The discount is underwhelming on purpose. The brands who made Dover's shelves possible are last in line to see any of the proceeds. And the Texas stores that have not yet announced their closures are not an exception. They are a paperwork problem.

Dover's three Texas locations, in Dallas, Austin, and Houston, have not announced closures. That is not ambiguity about their fate.

Texas law requires more than filing paperwork. Under Texas Business and Commerce Code Section 17.83, a retailer cannot conduct a going-out-of-business sale until it has filed an original inventory with the chief appraiser of the local appraisal district. That inventory must be complete and detailed, listing every item of goods, wares, and merchandise to be offered on the opening date of the sale along with the total cost of those items. It must be submitted as a sworn affidavit. The application cannot be considered until that inventory is in hand.

Only after the chief appraiser receives and approves the original inventory is a permit issued. The permit is valid for 120 days and is not renewable.

What that means in practice: before a Texas Dover location can advertise a single day of closing sales, someone has to physically count and document every item in the store, swear to its accuracy before a notary, and wait for the county appraisal district to issue a permit. That is not a filing delay. That is operational work that has to happen on the ground first. The outcome for those three stores is the same as every other location. The process just requires more steps to get there.

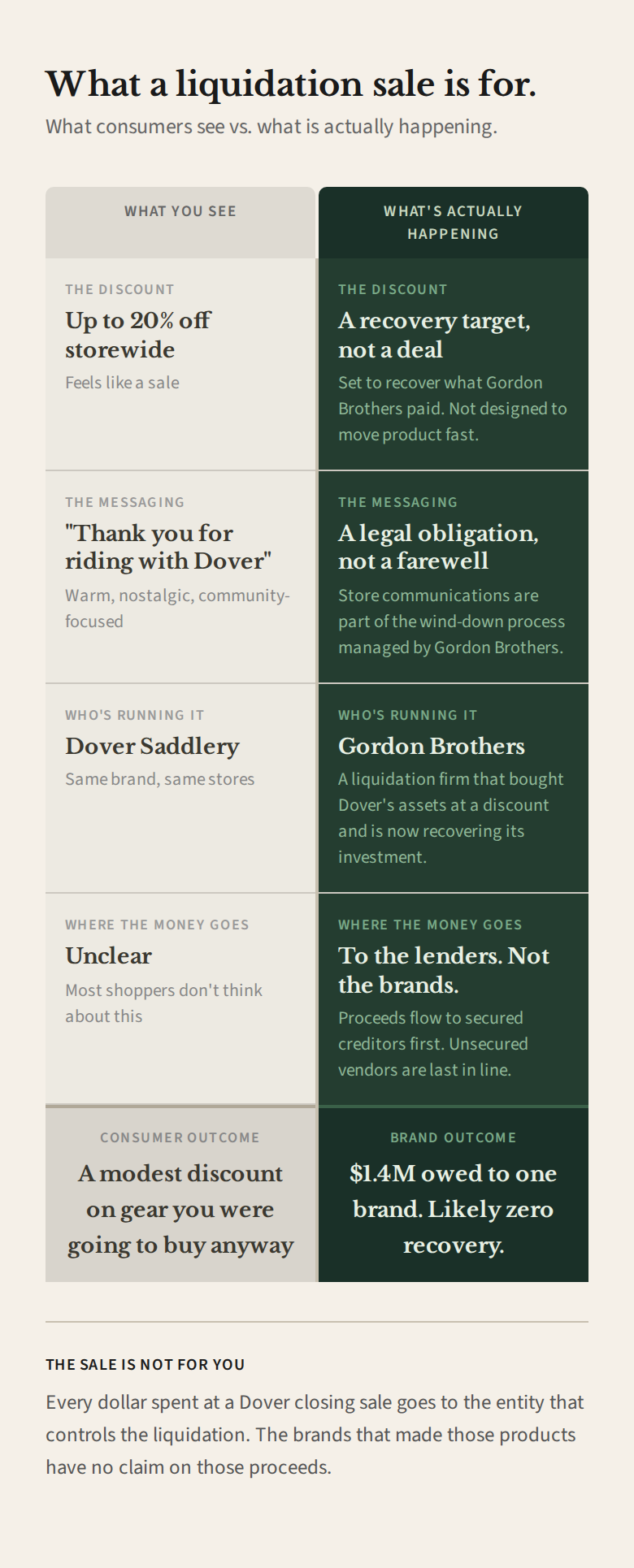

Dover stores are advertising up to 20% off storewide. For a going-out-of-business sale, that is a shallow discount. Retail liquidations typically open at 40 to 80 percent off. A 20 percent discount does not reach the floor of what analysts classify as clearance pricing, which runs 20 to 40 percent. If you walked into a Dover store expecting genuine liquidation pricing, the gap between expectation and reality is not an accident.

Gordon Brothers did not acquire Dover to serve equestrian consumers. It acquired Dover's inventory assets at a discount from Prudential Financial's lending arm, which had taken over the company from private equity firm Promus Equity Partners after control transferred to its lenders. Gordon Brothers' job is to recover enough from the liquidation to make a profit on what it paid. A 20% discount is calibrated to that recovery target, not to move product quickly.

This is how asset-based lending liquidations work. The discount you see reflects the lender's math, not the retailer's urgency. If the opening discount were deeper, Gordon Brothers would recover less. So it is not deeper.

The publicly known credit facility is a $15 million revolving line from Second Avenue Capital Partners, secured in August 2024. But that figure almost certainly understates Dover's total debt exposure, for reasons that are structural to how asset-based lending works.

Start with a concept most people already understand.

Think of a credit card. You have a limit, you spend against it, you pay it down, you spend again. A revolving credit facility works the same way, with one critical difference: the limit is not fixed. In an asset-based lending structure, the maximum Dover could borrow at any given moment was tied directly to the value of inventory sitting on its shelves. The more inventory on hand, the higher the limit. The less inventory, or the older it got, the lower the limit.

That mechanic creates a specific incentive. For a retailer actively expanding, with a flagship location planned at the World Equestrian Center in Ocala and a franchising program in development, keeping shelves stocked was not just a retail decision. It was a financing decision. High inventory meant a higher borrowing limit. A higher borrowing limit, drawn against, funded operations.

Here is how that unravels.

Using round numbers for illustration:

- Dover holds $20 million in inventory. The lender allows borrowing up to 60% of that value, so the borrowing base is $12 million.

- Sales disappoint. Inventory does not convert to cash. Dover draws $11 million to cover operations and does not pay it down.

- Inventory ages on the shelf. The lender applies what is called an advance rate haircut: older product counts for less. The borrowing base drops to $8 million.

- Dover's outstanding balance is $11 million. The borrowing base is $8 million. That $3 million gap is called a borrowing base deficiency.

- A borrowing base deficiency is a technical default. The lender can call the loan.

Interest accrues on the outstanding balance throughout this process. The deeper the inventory ages and the more sales disappoint, the faster the gap widens.

The Boston Globe reported that before Gordon Brothers came in, Dover was taken over by its primary lender, described as an arm of Prudential Financial. That appears to be a separate facility from Second Avenue's $15 million line, which suggests the actual total debt obligation was larger than the one publicly reported number. The full capital structure has not been disclosed.

Multiple sources with direct knowledge of vendor operations have told me that two things were happening simultaneously at Dover starting in October and November 2025:

- Dover stopped paying a significant portion of its vendor base.

- Dover continued issuing purchase orders and requesting that brands keep shipping inventory.

To be precise about sourcing: the payment stoppage and the continued PO issuance are reported to me by industry sources. What follows is my analysis, not confirmed fact.

The behavior is consistent with a company trying to maintain its borrowing base as long as possible. Recall the mechanic from above: incoming inventory raises the eligible collateral pool, which keeps the borrowing limit higher. If Dover was no longer paying for that inventory but was still receiving it, it was using vendor financing to prop up its borrowing capacity. The brands extended good-faith credit to an institution that was already in default on its payment obligations to them.

That inventory is now on Dover's shelves. Gordon Brothers is selling it. The vendors who shipped it have not been paid.

Earlier this year, when the first wave of store closures was announced, store employees with direct knowledge of operations told me that affected locations were given approximately 48 hours notice and directed to pack remaining inventory and ship it to other stores. The goal was to keep shelves full at the stores that were staying open.

That behavior is not present in the current round of closures.

The contrast is instructive. In the first wave, there were still stores worth keeping stocked. Consolidating inventory to those locations served a purpose: it maintained shelf presence, and it kept eligible inventory concentrated at active locations, which matters for borrowing base calculations. The behavior was consistent with a company still trying to extend its operational life.

In this final round, there is nowhere to send the inventory. Gordon Brothers is running simultaneous liquidations across all locations. Everything sells in place. The shift from consolidate-to-survive to liquidate-in-place is the clearest possible marker that no operational future was ever on the table once Gordon Brothers came in.

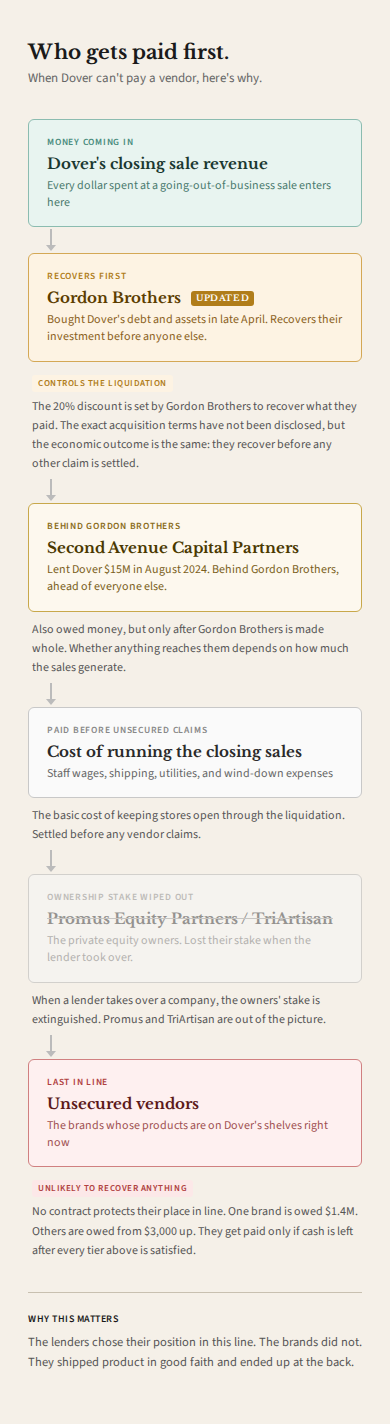

When a liquidation of this structure runs, the proceeds move through a priority waterfall. Here is the order:

- Gordon Brothers recovers first. Having acquired Dover's assets through Prudential Financial's lending arm, Gordon Brothers recovers its investment before any other claim is settled. The exact terms of the acquisition have not been publicly disclosed, but the economic outcome is the same regardless of structure.

- Second Avenue Capital Partners. Dover's $15 million revolving credit lender sits behind Gordon Brothers but ahead of unsecured creditors. Whether any proceeds reach this tier depends on what Gordon Brothers paid for the assets and what the closing sales generate.

- Administrative costs. The cost of running the liquidation itself: staff wages, freight, utilities through closure.

- Unsecured trade creditors last. This is where the brands sit.

Any vendor who extended Dover net-30 or net-60 terms is an unsecured creditor. In a liquidation waterfall, unsecured creditors recover whatever is left after everyone ahead of them has been made whole. In most retail liquidations of this kind, that means cents on the dollar, if anything.

The Plaid Horse reported in May 2026, drawing on conversations with multiple affected companies, that one brand is owed $1.4 million in unpaid invoices for product that was shipped, received, placed on Dover's shelves, and never paid for. The range across the vendor base is wide:

- Smaller vendors are owed amounts starting around $3,000.

- Mid-size manufacturers are reporting losses in the mid-to-high five figures.

- Several companies have disclosed losses in the mid-to-high six figures.

- One brand is owed $1.4 million. That is the largest single known claim.

That product is on Dover's racks right now. Some of it is selling at 20% off. None of those proceeds go to the brands that made it.

The Plaid Horse piece is worth reading in full. They did the reporting. The link is here.

The 20% discount is not a shopping event. It is a data point. It tells you the price at which Gordon Brothers calculated it could recover its acquisition cost and turn a profit. It tells you that the liquidation was designed around a lender's math, not a consumer's benefit. And it tells you that every dollar spent at a Dover closing sale goes to the entity at the top of the creditor waterfall, not to the brands at the bottom.

If you are an equestrian brand and Dover was a meaningful part of your distribution, this is the moment to understand what your exposure looks like. Your outstanding receivables are an unsecured claim in a completed liquidation. The legal and financial steps worth taking now are a conversation for your counsel, not this article. But the picture is clear enough to act on.

The equestrian industry has a habit of processing these collapses as betrayals by beloved institutions. Dover earned its reputation over fifty years, and that reputation was real. But the institution that built it and the financial structure that dismantled it are not the same thing. Understanding the difference is the only way to avoid standing at the back of the waterfall next time.