In the past three months, I've watched five horse industry headlines get treated as five separate stories. They're not. They're the same story, and most of the industry is reading it wrong.

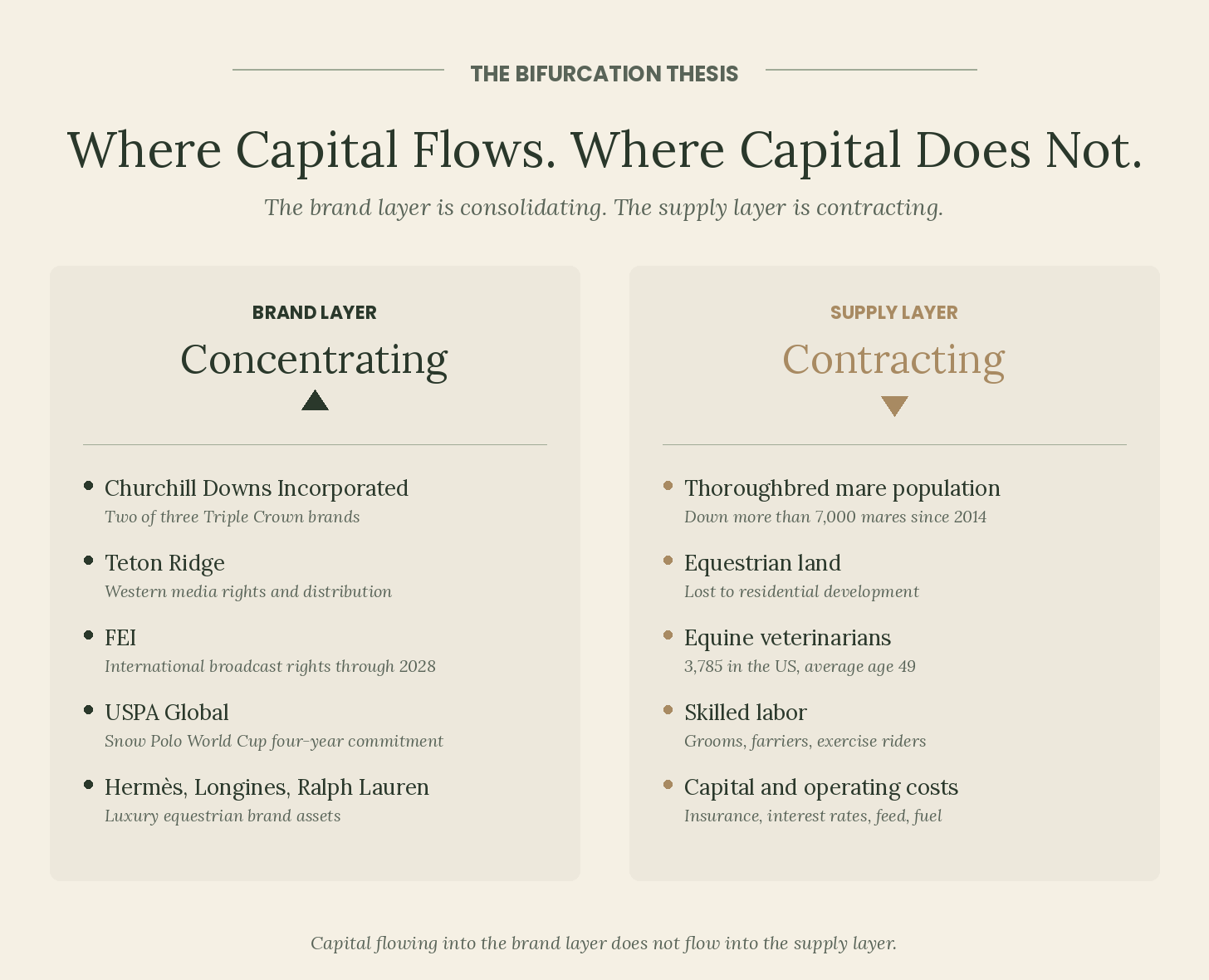

What's actually happening: Capital is concentrating in the brand and intellectual property layer of the horse industry. The supply layer of breeders, trainers, veterinarians, diagnostic labs, and operating facilities is contracting. The split is happening because distribution and rights can be hired and operating depth cannot.

Meanwhile, the cost of participating in this industry has outpaced household income for two decades. Take the amateur owner with one or two horses on a hunter/jumper schedule, the small-scale breeder running a handful of mares, the working professional competing at the AA level. Their incomes haven't kept pace with what it costs to participate: board, training, vet care, show fees, hauling, and replacing horses every five to seven years. As that participation base contracts, the businesses serving it contract too. The demand side and the supply side of the middle market are getting smaller at once.

This pattern is visible simultaneously across thoroughbred racing, Western performance horse, English sport horse, and polo. It is not just American. It will define which operators win and which lose over the next five years.

If you breed, train, sell to, or invest in any part of this industry, the structure of the business is changing under your feet.

- April 22, 2026: Churchill Downs buys the Preakness IP. Churchill Downs Incorporated agreed to acquire the trademark and brand rights to the Preakness Stakes and Black-Eyed Susan Stakes from 1/ST Racing for $85 million, with the rights to be licensed back annually to the state of Maryland. CDI is buying the IP; Maryland keeps the operations through the Maryland Stadium Authority and a nonprofit Maryland Jockey Club. Two of three Triple Crown brands are now under one publicly traded media-and-rights holder, with the operating side held by the state and the actual breeding of Triple Crown-eligible horses happening at Coolmore, WinStar, Lane's End, and a handful of other commercial breeding operations.

- April 15, 2026: Etalon Diagnostics liquidates. A Silicon Valley-backed equine genetics company that had raised approximately $18 million in late 2022 liquidated through a California Assignment for the Benefit of Creditors three years and four months after closing its Series A. The lead investors were Thomas Tull and Teton Ridge, and the Series A added a former Hulu and Fox Networks executive to the board, which is the kind of director you place on a content company, not a science company. I read Etalon as having been positioned as the data layer of a Western lifestyle content empire as much as a diagnostics company, and when that broader thesis fell apart, the diagnostics arm had no independent rationale.

- February 11, 2026: The FEI signs a broadcast rights deal with China Media Group. The international governing body for equestrian sport finalized a multi-year media rights partnership with China's premier state broadcaster covering the FEI World Championships 2026, FEI European Championships 2027, FEI Jumping World Cup, Longines League of Nations, and FEI Eventing Nations Cup through 2028. The deal is pure rights monetization: no operational commitment, no horseman-side investment, no claim on the supply layer. Five weeks later, Hermès staged its sixteenth Saut Hermès at the Grand Palais in Paris, the latest example of a luxury house using show jumping as a vehicle for brand expression in a flagship cultural venue.

- February 2026: Teton Ridge unwinds the operating side. Sports Illustrated reported that Teton Ridge had canceled the 2026 American Performance Horseman, the latest move in an eighteen-month unwind that included a $28 million dispersal of 116 head of breeding and performance horses, the sale of TR9 Ranch to Theorem Ranch, and Etalon's liquidation. What Teton Ridge has kept: the Cowboy Channel, the PRCA exclusive licensing deal, The American Rodeo, C&I Magazine, and the Lonesome Dove development deal. The company that spent 2019 to 2024 building a vertically integrated Western lifestyle portfolio is now a sports rights and distribution business run by a CEO whose career was Outsider, Barstool, MLB, ESPN, and Yahoo, which is a perfectly rational team for the business they have decided to be in.

- January 23-25, 2026: The Snow Polo World Cup St. Moritz. The forty-first edition drew 26,000 spectators to a frozen Swiss lake supporting 2,400 tonnes of installed infrastructure for three days of high-goal polo, while USPA Global confirmed a four-year sponsorship commitment to the event. Robb Report's coverage led with private jets, Birkin bags, and Mackage puffers; the horses were background. The labor and breeding economy that makes high-goal polo possible operates largely outside the brand frame, in countries and supply chains that get none of the luxury attention.

The supply layer is contracting in parallel across every segment, the same way the brand layer is consolidating. The deep dives go into each in detail. The headline signals are visible now:

- Breeding contraction. The Report of Mares Bred has fallen from 34,121 in 2014 to 27,180 in 2024, a decline of more than 7,000 mares in ten years, and the 2025 foal crop is projected at 17,300, down 3.4 percent year over year.

- Land and real estate. Equestrian land near growing metro areas (Wellington, Ocala, Lexington, Aiken, Middleburg) is being lost to residential development. The Wellington Lifestyle Partners golf community development on the former Equestrian Preserve land is the most visible recent example. The agricultural land that remains carries rising property taxes, lease costs, and zoning friction that compounds the cost of operating any facility at scale.

- Labor pipeline. The 2024 AAEP/AVMA report counts roughly 3,785 equine-exclusive practitioners in the United States with an average age of 49 and only 1.3 percent of new vet graduates entering equine practice, and the same shortage dynamics are playing out across farriers, grooms, exercise riders, and barn managers, much of which has historically depended on labor pools now under immigration policy pressure.

- Capital and operating costs. Equine insurance premiums and liability costs are rising, interest rates are making farm financing and breeding operations harder to capitalize, and feed, hay, fuel, and construction costs have not come down from their 2022 highs.

- The European warmblood arbitrage under pressure. The opportunity for US amateur buyers to source quality sport horses from Europe at affordable prices has narrowed over the past decade as European prices rose, the dollar weakened against the euro at sustained intervals, and the supply of well-produced horses in the amateur price band thinned out at home.

"Distribution and rights can be hired. Operating depth cannot."

Five deep dives follow:

- Thoroughbred Racing. The CDI and Preakness deal in full structure, the foal crop trajectory and what the 17,300 number means for the racing economy, the Maryland experiment as a model for state operation of racing assets, and the concentration of commercial breeding to a handful of operations.

- Western and Quarter Horse. The Teton Ridge unwind in full operational detail, the AQHA futurity economy, and the cutting and reining circuits, including why the September 2025 dispersal economics matter beyond Teton Ridge.

- English Sport Horses. The collapse of the European warmblood arbitrage opportunity for US amateur buyers, USEF and USHJA governance under contracting amateur participation, the luxury house investment in show jumping, and the in-person experience layer that does not yet scale.

- Labor and Policy. The equine veterinarian pipeline crisis, immigration policy effects on grooms and farriers, the regulatory environment around HISA and FEI welfare standards, and the insurance market exit.

- Who Wins by 2031. An evolving hypothesis on the operators best positioned to win the next five years and the attributes that define them. Sharpened by the deep dives that come before it.

The cultural moment for horses is real. The supply chain that produces those horses is genuinely struggling. Both things are true at the same time, and the relationship between them is the most important question in the industry.