"When Roy was building the business, there was Charles Owen and there was Champion. There was two big brands and they sold every hat. Now, there's 200 brands. And we've all got a much smaller piece of the pie than we had."

That is Dave Derby, CEO of Charles Owen, speaking on a recent episode of the Shut Up and Ride podcast. It is the most important public statement anyone in the equestrian manufacturing industry has made in years.

The context matters. Shut Up and Ride is sponsored by Charles Owen. The episode was a brand-controlled communication surface. The hosts work with a commercial relationship to the guest's company. Read the Derby quotes in this piece with that in mind. Leaders tend to be more candid in friendly rooms than in hostile ones, and what Derby said in that room is more revealing than what he would have said to a reporter asking adversarial questions.

Not because it was rehearsed or strategic. It almost certainly wasn't. Derby was defending his company's decision to close UK manufacturing and move production to China, and the 200-brands line came out as a frustrated aside. But it describes, with precision, the economic condition that has been squeezing every UK legacy equestrian manufacturer for the last twenty years. And it explains why Charles Owen is closing its Wrexham factory regardless of whether the lease was renewed.

This is a structural story, not a personal one.

A Note on the Numbers

The financial detail in this article comes from two primary sources. The first is Companies House, the UK companies registrar, where all UK limited companies file annual accounts, director appointments and resignations, charges against assets, and changes in share structure. The filings are audited for larger entities (including COMFG Ltd, the main Charles Owen operating company) and unaudited for smaller ones (including EQX Ltd).

The second is charlesowen.com, audited in March 2026 for what the brand is publicly claiming about itself.

The podcast quotes come from a recent episode of the Shut Up and Ride podcast, hosted by eventing rider Simon Grieve, liberty trainer Ben Atkinson, and equestrian journalist Jenny Rudall, featuring Dave Derby (CEO) and Jade Dempsey (marketing) of Charles Owen. The podcast is sponsored by Charles Owen. The episode is a brand-controlled communication surface, not an adversarial interview. Derby's on-record admissions should be treated as reliable (people do not typically volunteer things against their own commercial interest, even on friendly podcasts). The hosts' framing and the questions they chose to ask, however, reflect a commercial relationship with the guest's company. Where quotes have been edited, it is for readability only, and the original wording is preserved in the research file.

Where claims cannot be verified from public records, I have flagged them as unconfirmed or unaddressed.

All figures from Companies House filings are in British pounds. US dollar equivalents in parentheses are calculated at the current mid-market rate of £1 = $1.35, rounded to three significant figures.

This piece is written as structural analysis, not consumer advocacy. The goal is to explain what the public record shows, what the brand's own leadership has said, and what both imply about the broader category. Readers can draw their own conclusions about the consumer-facing questions.

The Structural Squeeze

Specialty consumer categories do not stay concentrated forever.

In the 1980s and 1990s, equestrian helmet manufacturing in the English-speaking world was dominated by a handful of brands. Charles Owen and Champion were the two that Derby remembers. There were a few others. They supplied the vast majority of riding helmets sold in the UK and in the professional competition market globally.

Forty years later, the category looks completely different. Derby's "200 brands" number is directionally right for the global market once you include European brands (Samshield, KEP Italia, Casco, KASK, Uvex), US brands (Troxel, Ovation, One K, Tipperary), and the dozens of smaller specialty manufacturers that have entered since standards bodies opened up in the 1990s.

Fragmentation of a specialty category creates a specific economic squeeze on legacy manufacturers. The fixed costs of UK manufacturing (factory, workforce, regulatory overhead, certification costs) do not shrink when market share shrinks. Revenue per brand falls because the same demand is now divided across many more competitors. Inherited brand equity softens the revenue decline but does not eliminate it. And the economics of small-batch UK helmet production depend on volume that a fragmenting market cannot support.

None of this is specific to Charles Owen. Every UK legacy specialty manufacturer in equestrian is sitting on some version of this equation. The ones that have adapted (typically by moving production overseas while keeping design, testing, and brand in the UK) have a fighting chance. The ones that have not are running out of time.

Charles Owen is the visible case study because the company's numbers, structure, and leadership commentary are all publicly available. Most aren't.

The Financial Record

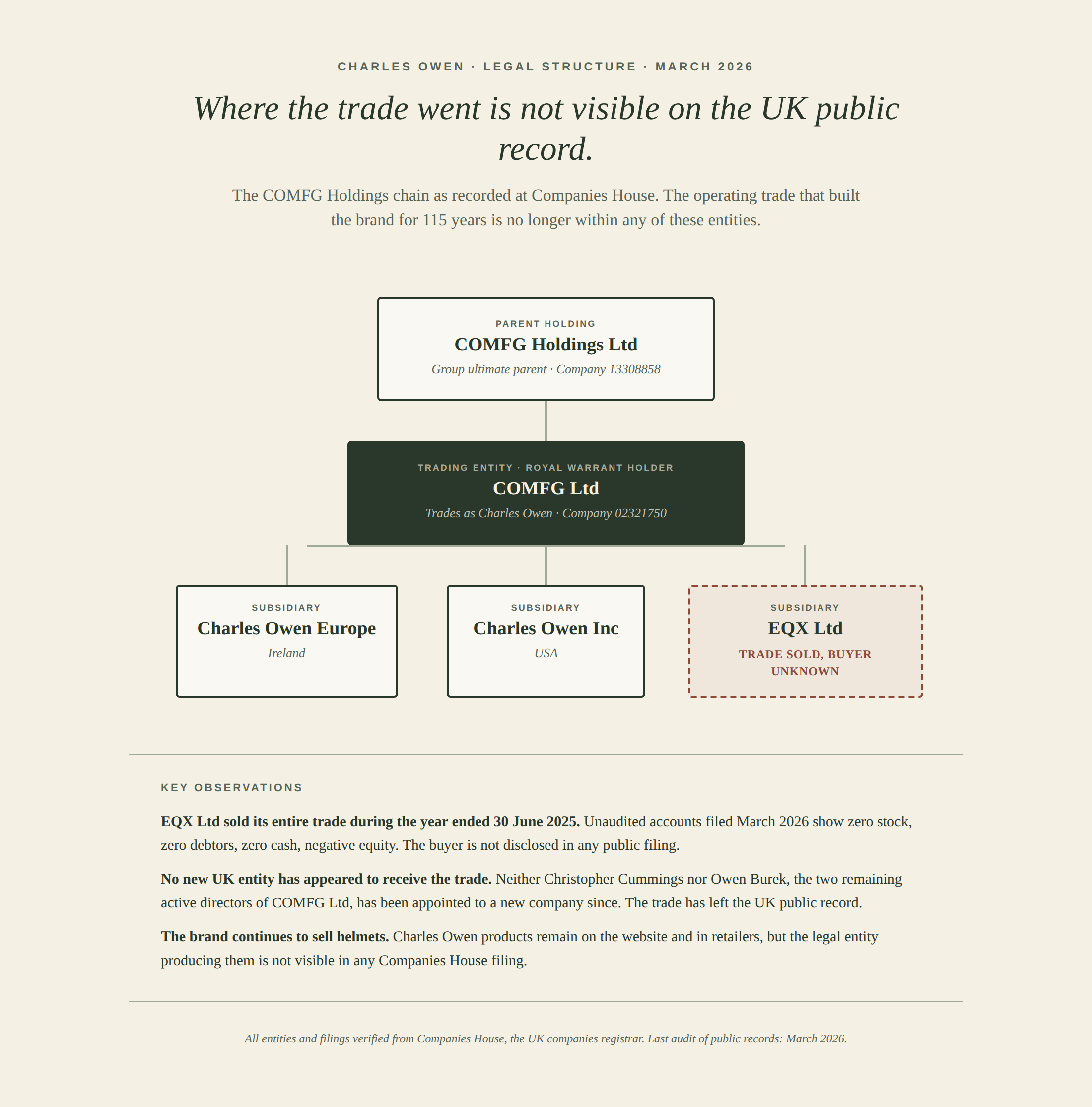

COMFG Ltd (company registration 02321750) is the UK operating entity that trades as Charles Owen. Its most recent audited accounts, for the year ended 30 June 2024, tell a clear story.

Total equity fell from £562,826 ($760,000) in June 2023 to £116,698 ($158,000) in June 2024. That is a £446,000 ($602,000) collapse in a single year. The company made a loss for the year, confirmed by the auditor's opinion. Cash fell from £309,858 ($418,000) to £47,788 ($65,000). Stock was run down from £630,808 ($852,000) to £332,569 ($449,000). On a standalone basis, the company was technically insolvent by year end, with current liabilities exceeding current assets by £680,639 ($919,000).

Short-term creditors at year end totaled £4.11 million ($5.55 million), of which £3.48 million ($4.7 million) was classified as "other creditors." This is a large liability (a third of group revenue) that has been sitting on the balance sheet for at least two years, consistent with intercompany debt or a long-standing loan.

The Wrexham property was sold during the year and rented back, initially from a connected party and subsequently, per the accounts, at what the filing describes as "a peppercorn rate" from an unconnected party. That transaction provided cash to pay down creditors, including Barclays Bank charges that were satisfied in December 2024.

In November 2024, COMFG Ltd took out new financing from Ultimate Finance Limited, a specialist asset-based lender. The charge covers all present and future freehold and leasehold land, all intellectual property, and all assets. It remains outstanding. Ultimate Finance typically provides working capital to companies that cannot access mainstream bank lending.

Twelve months later, in November 2025, the company announced it was closing its Wrexham factory.

The Leadership Commentary

The reported reason for the closure was the expiry of the factory lease. Dave Derby initially described the closure as a response to the inability to secure a new lease on the Wrexham premises.

On the Shut Up and Ride podcast, Derby added a structural frame to that explanation.

"I think going forward, to answer your question, I think at some point, somewhere in the distant future, we probably would have closed down the UK manufacturing anyway. The unfortunate property issue we had, we just accelerated it."

That is a significant admission. It reframes the closure from an unfortunate event triggered by a landlord to a long-planned restructure that happened on a timeline the company did not choose. Both framings can be true at once. The property issue was real. The decision to stop UK manufacturing was, by Derby's own account, directionally inevitable regardless.

Derby's defense of the decision is also structural. The company's first China-made product, the Kylo helmet, launched in May 2023, specifically for the badminton discipline. According to Jade Dempsey on the same podcast, the Kylo became the brand's best-selling product within four to five months, and "our biggest selling product that we'd made for probably the last 20 years." Eighteen months later, the Jockey School helmet was added to the Chinese-manufactured range.

In other words, by the time the factory closure was announced in November 2025, Charles Owen's top-selling product was already being made outside the UK, and had been for more than two years.

The Safety Question, Examined

Dempsey's defense of the safety of China-manufactured helmets is also structural. Prototypes are tested on the company's own test rig, sent to UK test houses for certification approval, and then batches are tested again after production. "If we felt those products that we design in the UK and have made out in the Far East were in any way less safe than any other brand, we wouldn't do it."

This is the formal safety position. Taken at face value, it is technically correct. Standards bodies certify helmets to specific impact, penetration, and retention tests. Those tests are independent of where the helmet was assembled. A China-manufactured helmet that passes the same certification as a UK-manufactured helmet is, by the governing standard, equally safe.

That is not the only question a careful consumer should ask.

Certification is a pass/fail threshold on a known design. It tells you that a helmet meeting the submitted specification performs within the standard at the moment of testing. It does not tell you whether the institutional knowledge that built the design still exists inside the company, whether the people who catch edge cases before they reach certification are still employed, or whether the quality control feedback loop between production and design is intact.

Charles Owen's safety reputation was built over several decades by specific people. Roy Burek, the Oxford-trained chemist who ran the brand from 1981 until his death in 2019, was a passionate advocate for equestrian safety standards and drove the company's investment in in-house research and testing. The Wrexham factory was not just a production site. It was the place where prototypes were made, tested, refined, broken, and remade, and where the people doing that work sat ten feet from the people designing the next model. That co-located research-and-production loop is a specific kind of organizational asset. It is not easily replicated by outsourcing production to a factory the brand does not own and does not staff.

The Wrexham factory closed on 19 December 2025. According to Companies House, CEO Dave Derby resigned as a director of COMFG Ltd on 18 February 2026. Ricky Hone, the operations director who had been on the board since 2012, resigned on the day the factory closed. Michelle Morris resigned the day after Derby. Michael Clarkson, the company secretary, resigned 27 February. The two directors who remain, Owen Burek and Christopher Cummings, are the family shareholder and the long-standing finance director respectively. Neither has the manufacturing or safety research background of the people who left.

Dempsey's on-record claim that the testing regime is unchanged is plausible and may be accurate. It is also not the same thing as the safety culture being unchanged. A culture is the sum of the people who carry it. A reporting relationship, a pre-certification peer review, an informal flag between a factory-floor technician and a design engineer, none of that transfers automatically when manufacturing moves to a contract facility and the senior operating team is replaced.

Related to this is the accountability question. Brand warranties, recall procedures, and product liability all sit with a specific legal entity. When a consumer buys a Charles Owen helmet today, the website terms of service identify COMFG Ltd as the legal seller. But COMFG Ltd's operating subsidiary, EQX Ltd, has disclosed in filed accounts that it sold its entire trade to an undisclosed buyer during the year ended 30 June 2025.

Derby's February 2026 resignation from COMFG Ltd does not end his involvement with the Charles Owen corporate structure. According to Companies House, Derby remains an active director of EQX Ltd, a position he has held since the company was incorporated on 4 May 2023. Christopher Cummings has held the same role since the same day. Owen Burek was appointed to the EQX board on 23 September 2025, three months before the Wrexham factory closed. All three are listed as current directors of the entity that disclosed selling its entire trade to a buyer it has not named.

That creates a gap. If a safety issue surfaces on a helmet sold today, the consumer's recourse flows through COMFG Ltd, which does not hold the operating trade. The trade that actually produces the helmets sits with an entity that is not named in any public filing. A recall, a warranty claim, a product liability suit, all of these would need to work out which legal entity is now responsible before any consumer protection kicks in. A standard corporate restructure resolves this by announcing the new trading entity publicly. Charles Owen has not done this.

Finally, there is the trust question. Charles Owen's Our Story page, live as of March 2026 (three months after the factory closure), still describes the brand as "a leading British manufacturer of riding helmets" and references the Wrexham facility in the present tense. A consumer who lands on that page today has no way to know from the brand's own communications that UK manufacturing has ceased, that the trade has been sold to an undisclosed buyer, or that the CEO and three other senior officers have departed. The formal safety defense Derby and Dempsey offered on the Shut Up and Ride podcast did not appear in the brand's public consumer-facing communications. Podcast appearances reach a niche industry audience. The consumer buying a helmet from charlesowen.com still sees the brand that existed in 2024.

This is not a claim that Charles Owen helmets currently in the market are unsafe. They carry current certifications, and certifications are the objective measure of whether a helmet meets the standard. The question is not about the helmets that passed the tests. It is about what a consumer can reasonably know about the organization now producing them, and whether the formal safety defense the company has offered is sufficient given how much else has changed.

Who Else Is in the Same Position

Charles Owen is not alone in the economic position it occupies. The structural squeeze (legacy UK manufacturing, fragmenting specialty category, eroding unit economics, strong brand equity that softens but does not reverse the decline) applies to several other British and European legacy equestrian manufacturers.

The companies most exposed share a common profile. They were founded in the mid-to-late twentieth century. They built their reputations on in-house UK or Western European manufacturing. Their annual revenue sits in the single-digit millions to low tens of millions, which is too small to support the fixed cost base of specialty manufacturing and too large to be run as a lifestyle business. Their brand equity is real but is not translating into pricing power fast enough to offset unit economics. Their family or founder ownership has either ended or is late in its generational transfer.

How many brands fit that profile? Probably a dozen to two dozen in the English-speaking equestrian market. Not all of them will close their factories in the next three years. But the ones that do will do so for the same structural reason Charles Owen did, with the same structural framing: the category fragmented, the economics stopped working, the timing was determined by factors outside their control.

The brands that survive this transition will look different. They will design and certify products in the UK or Europe, manufacture overseas, and invest heavily in digital capability and consumer relationship. The ones that do not will either be acquired at distressed valuations or will fade as the 200 brands absorb their share.

This is the part of the story the industry has not wanted to talk about, because it requires acknowledging that the golden age of UK specialty equestrian manufacturing is ending. That is uncomfortable to say publicly. But it is what Derby described, and it is what the numbers show.

What This Means for the Decade

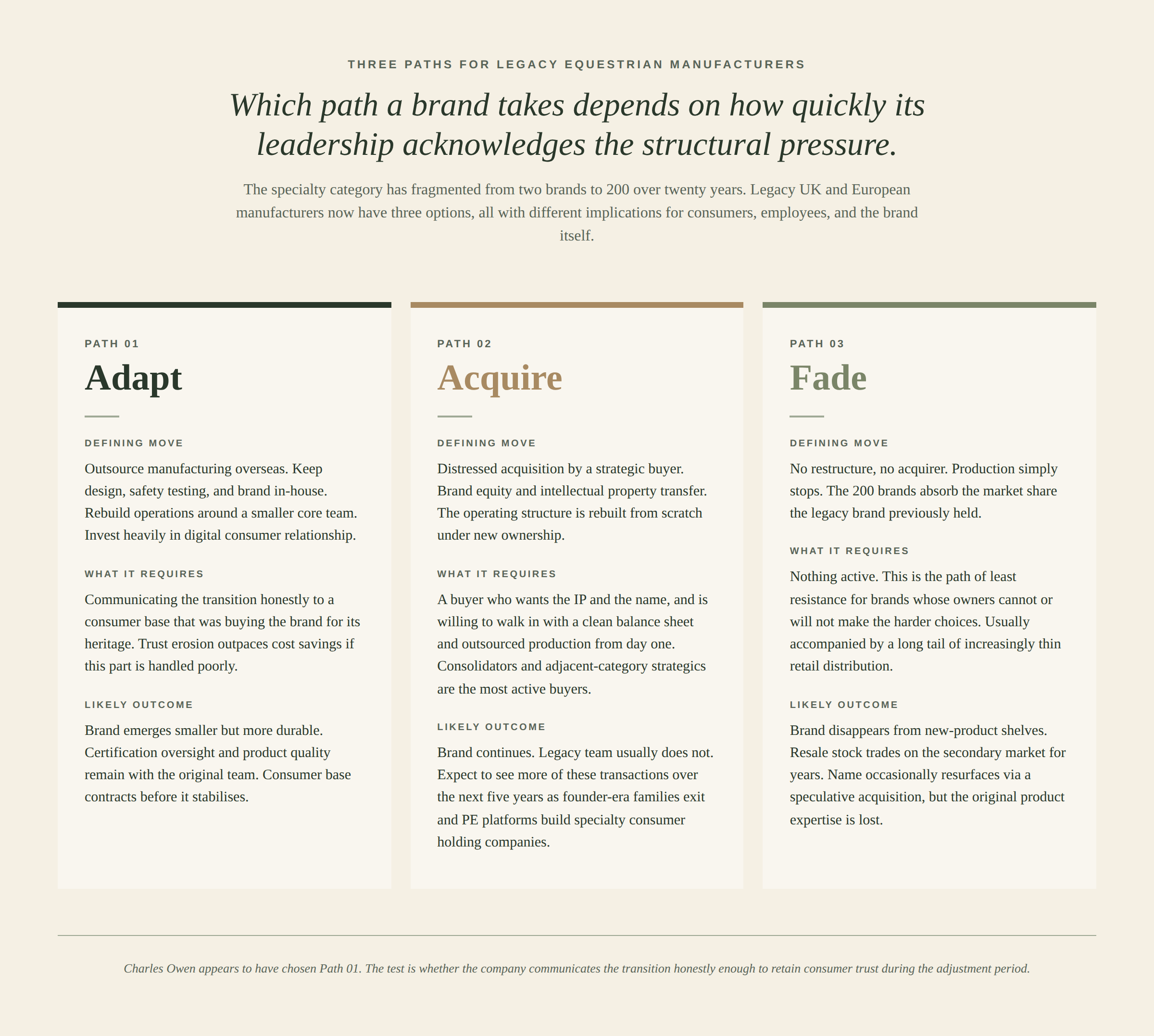

Three paths are available to legacy equestrian brands sitting in this structural position.

The first is what Charles Owen appears to have chosen: adapt to outsourced production, retain brand and design capability, rebuild the operating structure around a smaller core team, and invest in digital consumer relationship. This is the most difficult path, because it requires communicating the transition honestly to a consumer base that, in many cases, was buying the brand specifically for its UK manufacturing heritage. The brands that execute this transition well will emerge smaller but more durable. The brands that execute it poorly will find that the brand equity they were counting on erodes faster than their new cost structure can stabilize.

The second path is distressed acquisition. A legacy brand with strong equity but weak manufacturing economics is attractive to a strategic buyer who wants the IP and the name but can walk in with a clean balance sheet and outsourced production from day one. Expect to see more of these transactions over the next five years. The acquiring buyers will be a mix of consolidators, adjacent-category strategics, and private equity platforms building specialty consumer holding companies.

The third path is disappearance. Brands that cannot restructure and are not attractive enough to acquire will simply stop producing. The 200 brands will absorb their market share. The consumer will be offered a wider selection of technically competent helmets at a range of price points, with more emphasis on design innovation and less emphasis on heritage. Some of this is already happening.

For the consumer, the practical implication is that brand heritage is now a weaker predictor of product origin than it has ever been. The helmet bearing a hundred-year-old British name may be manufactured in the same Chinese factory that produces a newer brand's budget line. The certification is the same, but the provenance is not. That is neither good nor bad in safety terms. It is a shift in the meaning of what equestrian brands represent, and it will take the consumer market several years to adjust.

For the industry, the implication is that the structural pressure Derby described is not going away. It will continue to squeeze legacy manufacturers for the rest of the decade. The brands that adapt early and communicate honestly will hold their position. The brands that delay will find themselves having Derby's conversation in public on a timeline they did not choose.

That is the story Charles Owen tells, whether the company intended to tell it or not.

Orchid Bertelsen is an equestrian industry analyst and consumer marketing strategist with 20 years of experience in e-commerce and brand strategy. She rides at Grosse Pointe Equestrian in Michigan.